IRS Continues Targeting Poorest Families for More Tax Audits During FY 2022

Published March 29, 2022

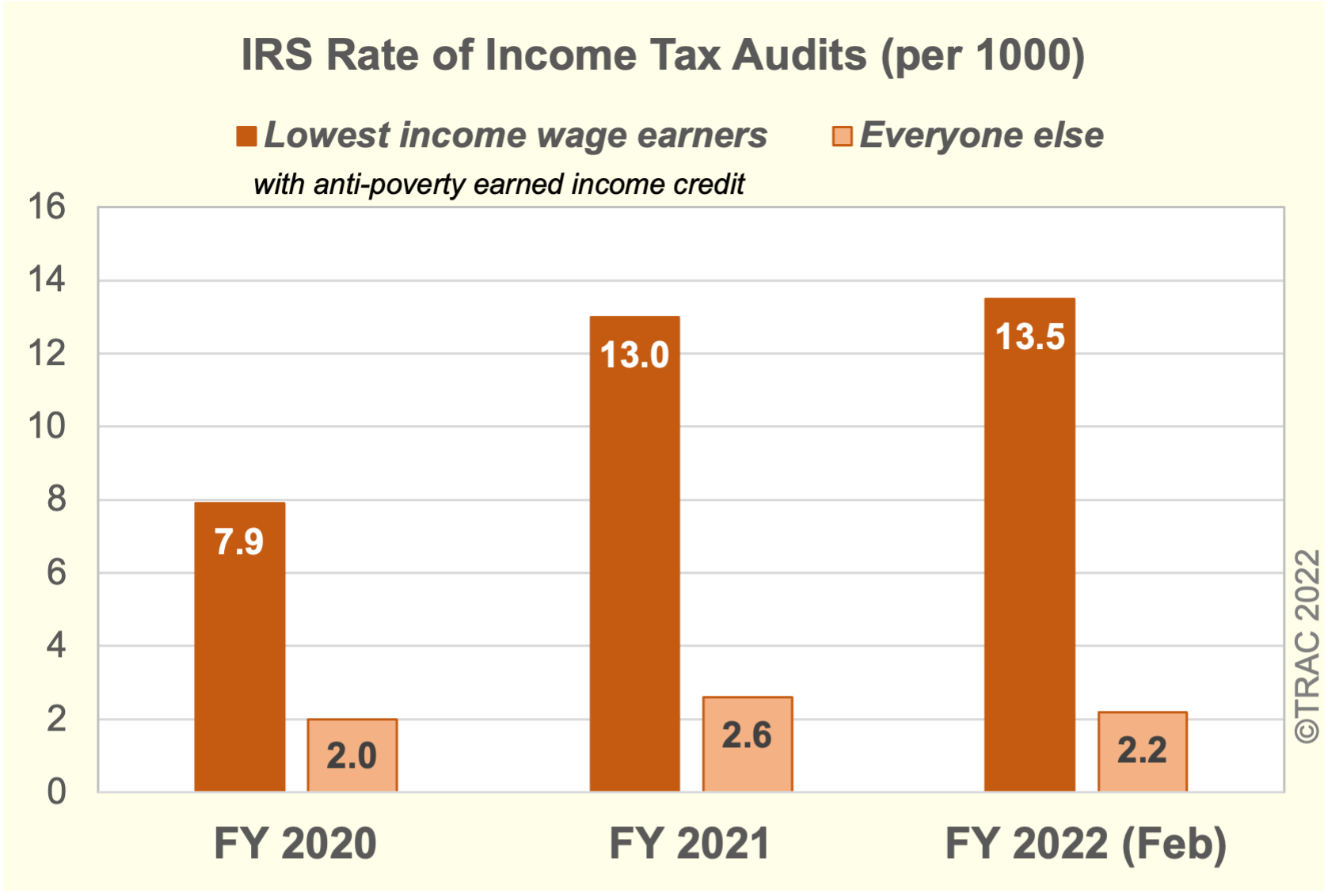

The latest Internal Revenue Service (IRS) statistics covering federal income tax audits through February of 2022 reveals that the agency is continuing to target audits on the poorest wage earners. So far it has completed 132,922 audits of these low-income wage earners with less than $25,000 in total gross receipts. This is up from 105,978 audits IRS had completed a year ago at the end of February 2021.

If IRS continues at this same pace for the rest of this fiscal year, audit rates would inch up to 13.5 per 1000 returns[1] – slightly higher than the phenomenally high rates that occurred last year when IRS audited the poorest families claiming an anti-poverty earned income tax credit at five times the rate for everyone else. See Figure 1 and Table 1.

Not only are total correspondence audits up so far this year, but IRS is increasingly targeting them on these poorest families. Last year at this same time, 51.6% of all correspondence audits (103,715 out of 200,856) were targeted at this lowest income group which represents only a small proportion of all taxpayers combined. The concentration of correspondence audits on this single small group of taxpayers during this filing season has increased to 58.1%, with the actual number of correspondence audits increasing to 130,106 out of 223,769.

In contrast, thus far during FY 2022 the number of correspondence audits dipped slightly for all other taxpayers. Compared with 97,141 audits of all other taxpayers completed at this time last year, as of February 2022, only 93,663 correspondence audits had been completed for everyone else aside from these poorest families who had declared an anti-poverty earned income tax credit.

A surprising finding from these internal IRS documents showed a similar pattern of increasing concentration of field audits to this lowest income group. Although much smaller in number, field audits were also up as of February 2022 on these low-income wage earners when compared to February 2021. In contrast regular face-to-face audits for all other taxpayers had slipped when February 2021 was compared to February 2022. See Table 2.

With only five months completed during this current fiscal year these figures only present a very preliminary picture of IRS enforcement efforts during this filing season. But the IRS’s own internal management statistics provide little evidence as yet that the IRS is not again forging ahead to target the poorest families at more than five times the rate for everyone else combined. [2]

| Category of Taxpayer | Return Filled | Return Audited | ||

|---|---|---|---|---|

| FY 2021 | FY 2021 (thru Feb) | FY 2022 (thru Feb) | ||

| Lowest income wage earners* | 23,620,209 | 306,944 | 105,978 | 132,922 |

| Everyone else | 136,457,242 | 352,059 | 134,271 | 126,193 |

| All taxpayers | 160,077,451 | 659,003 | 240,249 | 259,115 |

| Percent Lowest income wage earners | 14.8% | 46.6% | 44.1% | 51.3% |

| Category of Taxpayer | Correspondence Audits | Regular(face-to-face) | ||||

|---|---|---|---|---|---|---|

| FY 2021 | FY 2021 (thru Feb) | FY 2022 (thru Feb) | FY 2021 | FY 2021 (thru Feb) | FY 2022 (thru Feb) | |

| Lowest income wage earners* | 300,029 | 103,715 | 130,106 | 6,915 | 2,263 | 2,816 |

| Everyone else | 259,391 | 97,141 | 93,663 | 92,668 | 37,130 | 32,530 |

| All taxpayers | 559,420 | 200,856 | 223,769 | 99,583 | 39,393 | 35,346 |

| Percent Lowest income wage earners | 53.6% | 51.6% | 58.1% | 6.9% | 5.7% | 8.0% |

IRS Commissioner in State of Denial

IRS Commissioner Charles P. Rettig, appointed in October 2018 by then President Trump and serves for a five-year term as the head of the agency, testified March 17, 2022 before the Ways and Means Oversight Subcommittee of the U.S. House of Representatives. When he was asked about TRAC’s March 8, 2022 report, Commissioner Rettig angrily charged: “that report by Syracuse University is absolutely 100% false.” [3]

On March 21, 2022 we wrote Commissioner Rettig calling upon him to “publish the figures for individual income tax return examinations completed in Fiscal Year 2021. That way Congress and the public will be able to directly compare [his] 2021 figures against those contained in TRAC’s report covering FY 2021 and can decide for themselves whether the serious accusations you hurled were true or false.” The Commissioner has not responded to TRAC’s letter.

As the Commissioner well knew, TRAC’s reporting is based on the actual statistics IRS itself provides to us. TRAC obtains these figures directly from the IRS under a long-standing court order that requires the IRS provide internal management reports to us every month with detailed statistics on audits IRS is conducting. See Long et al v. United States Internal Revenue Service, USCDC WAW, Case Number 2:1974CV00724.

Back in 1974, shortly after the Freedom of Information Act was passed, the IRS had refused to release this information until Long’s series of court actions. Since this successful litigation by TRAC’s co-founder, the IRS began including current audit statistics in its annual reports. Unfortunately, IRS recently discontinued publishing these figures. For the first time, these statistics on completed IRS audits for the latest year were omitted from its FY 2020 Data Book. Commissioner Rettig thus far appears unwilling to publish these more recent statistics on the actual numbers of IRS audits completed by examination class.

How IRS Conducts Audits of Low-Income Taxpayers Is Fundamentally Unfair

The National Taxpayer Advocate, Erin M. Collins, in her annual report to Congress explained:

"Taxpayers require basic support and guidance from the IRS to fulfill their filing obligations and

pay amounts legally due. Phone service is an essential component of support and guidance... Without

support, taxpayers are disadvantaged and frustrated, and tax compliance is jeopardized."

Taxpayer Advocate Collins also has noted that correspondence audits are “one of the most significant tools the IRS employs to pursue compliance with tax laws.” And she went on to explain: “If the IRS does not receive a response, it will generally disallow the item(s) claimed and ultimately issue a Notice of Deficiency.”

Week-by-week the IRS determines the number of correspondence audits it will conduct. However, the agency “determines the number of planned [correspondence] audits based on the number of full-time equivalent (FTE) employees assigned to the IRS’s correspondence audit programs without regard to the volume of calls these audits will generate.” Yet the “staff conducting these audits must also staff the correspondence audit toll-free telephones.” See 2021 National Taxpayer Advocate Annual Report to Congress.

Despite the inadequacy of staffing of its phone lines, it appears that IRS is forging ahead to increase the number of correspondence audits so far during this current filing season. And as we see above in Table 2, the agency is increasingly targeting these on the poorest wage-earners. Taxpayer compliance is jeopardized not just when taxpayers underreport their tax liability, but also when IRS acts to unilaterally grab a taxpayer’s refund without cause. Increasing the letters (“correspondence audits”) IRS sends out without ensuring that it has the capacity to answer taxpayers’ calls on these audit letters, especially for low-income taxpayers who generally cannot afford tax accountants to assist them, is fundamentally unfair.

IRS’s own studies show that about 22 percent of taxpayers entitled to take the anti-poverty earned income tax credit fail to do so. If IRS was actually interested in treating taxpayers fairly,[4] it ought to consider sending some of these correspondence audit letters to these taxpayers who failed to claim the credit, letting them know that they may qualify for a refund or government payment, and providing them with an adequately staffed toll-free number to call if they want to learn more.